Financial services sector has been mostly impervious to

radical technical and business model changes. They have been able to maintain a

relatively stable but profitable business models over the last few decades.

Traditional business are now under siege from a whole host of innovators and

technology changes that are forcing a re-think on the business models of

traditional financial services sector.

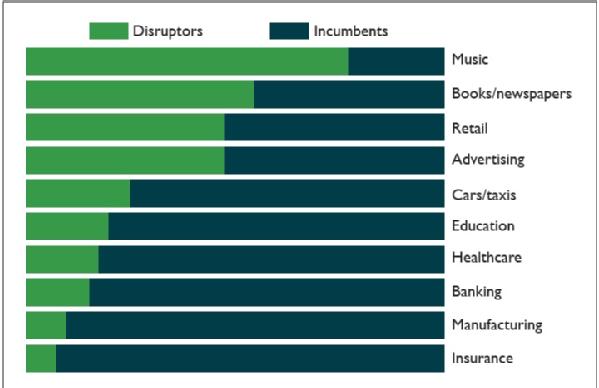

According to the World Economic Forum reports the impact is

felt across all sectors of the financial services industry.

Courtesy: WEF Report

According to the findings today’s innovators are different

from earlier disruptors in this sector for the following reasons:

- Today’s innovators are targeting the intersection of highly profitable business and customer’s area of frustrations and pain. Case being example International Money transfers. I have personally experienced it first-hand. In UK, high street banks charged from GBP 17, if done at bank to GBP 12 if done online for International Bank transfers to India and took 4 -5 business days to credit the account in India. In came innovators like Money2India and the same could be done at a fraction of the cost less than GBP 5 per transfer and credited in 1-2 business days to the account in India. This was a huge loss of such profitable business by high street banks to such innovators and the benefits to the customers.

2. The innovators are also using their technical

skills to automate manual processes that are currently very resource intensive.

“Robo-advisors” likes of Wealthfront, FutureAdvisor and Nutmeg have automated a full suite of wealth

management services including asset allocation, investment advice and even

complicated tax minimization strategies, all offered to customers via an online

portal. This allows them to offer services to a whole new groups of customers

that were once reserved for the elite. You do not need a six figure asset pool

to be eligible for such services .As a result, a whole new class of younger,

less wealthy individuals are receiving advice and support.

3. Use of Data and Analytics strategically has

been one of the key innovations of the new entrants to banking and insurance.

Traditionally Bankers would look at credit scores and insurance providers look

at health record or driving records. However, as our devices and social lives

are getting more entwined, the innovators are mining the data across devices

and social media to provide customized services. Some innovative insurers are

providing fitness bands to customers and based on whether you have been hitting

the couch or the gym regularly you have option of reducing your insurance

premiums. These sort of innovations have added a whole new set of customers.

With connected cars and more wearables and social connections, customized

products will become the norm.

4. Inspired by companies like Uber and Airbnb,

these innovators have learned to exploit the platform based capital light

models to grow revenues exponentially and keep costs nearly flat. The growth of

companies like Prosper and Lending Club are such examples having crossed

Billion dollars in origination transactions. Without putting their own capital

at risk, they have provided a market place for lenders and borrowers to meet

and avail the best rates. Similar has been the disruptive effort of

crowdfunding platforms that have helped start-up many new businesses that would

otherwise been not considered for funding by traditional banks and institutions.

5. As part of the growth strategy these innovators

are co-operating with incumbents in some areas and competing in some areas.

They are quick to take advantage of the scale and reach of these companies and

for traditional companies it is an easier channel to new markets. Like ApplePay,

is not competing with Visa and MasterCard but working with them on the payment

networks. Same is evident in India with innovators like paytm, oxigen, etc

tying up with traditional network and co-operating as a strategy to increase

their reach and growth.

The innovations and these changes can only

prove beneficial to end users in terms of better rates, efficient service and

customized attention from the providers.